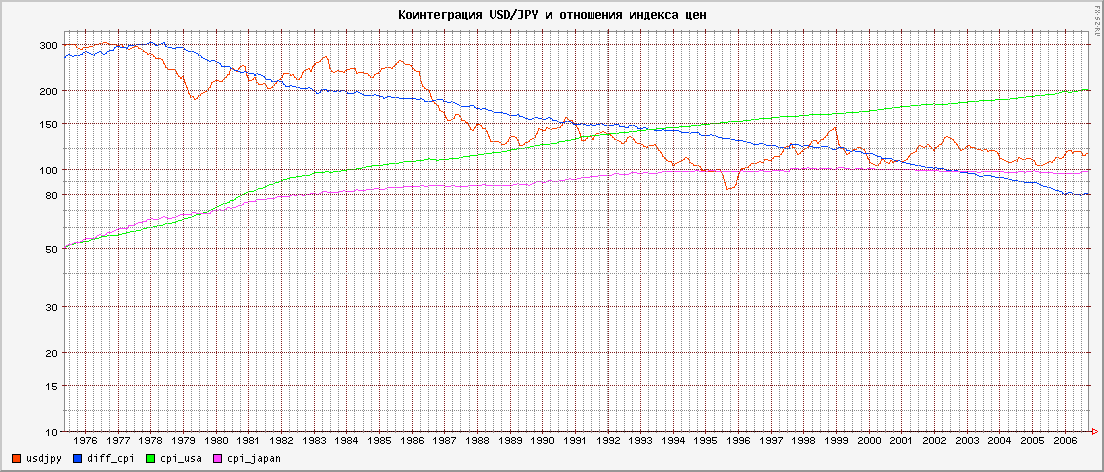

Step 3: cointegrating regression

Cointegrating regression -

OLS estimates using the 412 observations 1971:01-2005:04

Dependent variable: l_exjpus

VARIABLE COEFFICIENT STDERROR T STAT P-VALUE

const 5,60902 0,0176436 317,906 <0,00001 ***

cpi_diff 1,64565 0,0493659 33,336 <0,00001 ***

Unadjusted R-squared = 0,730488

Adjusted R-squared = 0,729831

Durbin-Watson statistic = 0,020749

First-order autocorrelation coeff. = 0,981198

Step 4: Dickey-Fuller test on residuals

Augmented Dickey-Fuller tests, order 12, for uhat

sample size 399

unit-root null hypothesis: a = 1

test without constant

estimated value of (a - 1): -0,022759

test statistic: t = -3,00329

asymptotic p-value 0,02689

P-values based on MacKinnon (JAE, 1996)

There is evidence for a cointegrating relationship if:

(a) The unit-root hypothesis is not rejected for the individual variables.

(b) The unit-root hypothesis is rejected for the residuals (uhat) from the

cointegrating regression.